281

Accounting Information Systems

Chapter 9 Appendix

Appendix 9A: Special Journals and Periodic Inventory

Special journals and subledgers can also be used if the company uses the periodic inventory system

instead of the perpetual inventory system. Most of the processes covered in chapter 9 still apply.

This includes posting totals at the end of the month to the appropriate general ledger accounts,

immediately posting amounts in the Other column to the general ledger accounts, and updating

the accounts receivable or accounts payable subledger accounts.

The difference lies in the accounts used in the special journals. Remember, the periodic inventory

system does not update inventory or cost of goods sold until a physical count is performed at the

end of the period. Thus, the sales and cash receipts journals will not update inventory or cost of

goods sold when a sale is made. Also, the purchase and cash payments journal will use purchases

and purchase discounts instead of inventory.

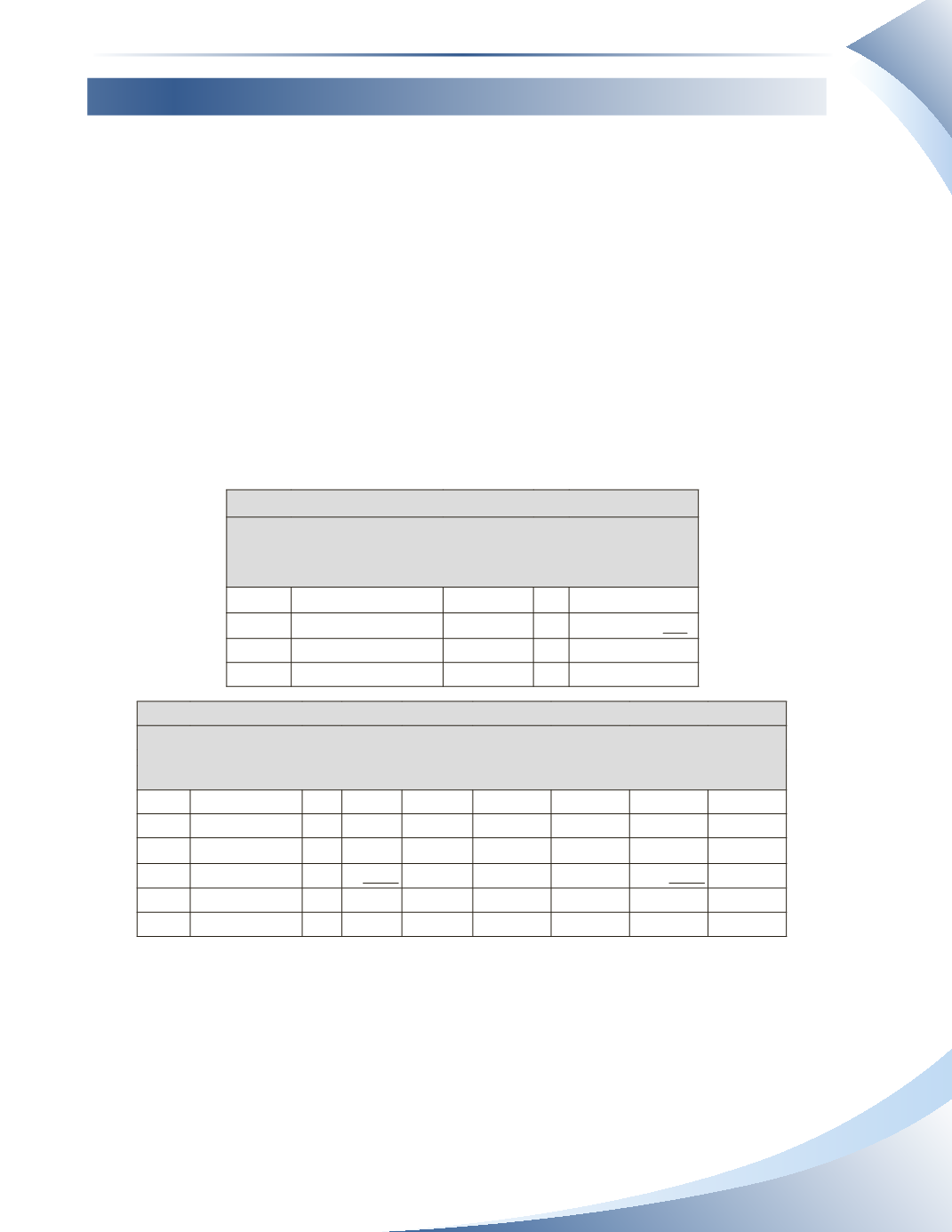

Figure 9A.1 illustrates the special journals for a periodic inventory system using the same sample

transactions used in chapter 9.

Sales Journal

Page 1

Date

Account

Invoice # PR

Accounts

Receivable/Sales

(DR/CR)

Jan 5 Joe Blog

5125

1,235

Jan 16 Furniture Retailers

5126

956

Jan 31 Total

$2,191

(110/400)

Cash Receipts Journal

Page 3

Sales Accounts

Bank

Cash Discount Receivable Sales

Loan Other

Date Account

PR (DR)

(DR)

(CR)

(CR)

(CR)

(CR)

Jan 2 Cash Sale

350

350

Jan 4 Owner’s Capital 300 4,000

4,000

Jan 10 Joe Blog

588

12

600

Jan 22 Bank Loan

2,000

2,000

Jan 31 Total

$6,938

$12

$600

$350 $2,000 $4,000

(101)

(405)

(110)

(400)

(220)

(X)