272

Chapter 9

Accounting Information Systems

Remember that at the end of the month, when the general ledger is updated by the journals,

the total of all the subledger accounts must equal the balance of the appropriate control account

(accounts receivable or accounts payable).

To prove that the total of the individual subledger accounts is equal to the respective control

account balance in the general ledger, a reconciliation is prepared. From Figure 9.11, the balance of

accounts receivable was $1,591. By finding the total of the accounts receivable subledger account,

we can prove that the control account and subledger are in balance.

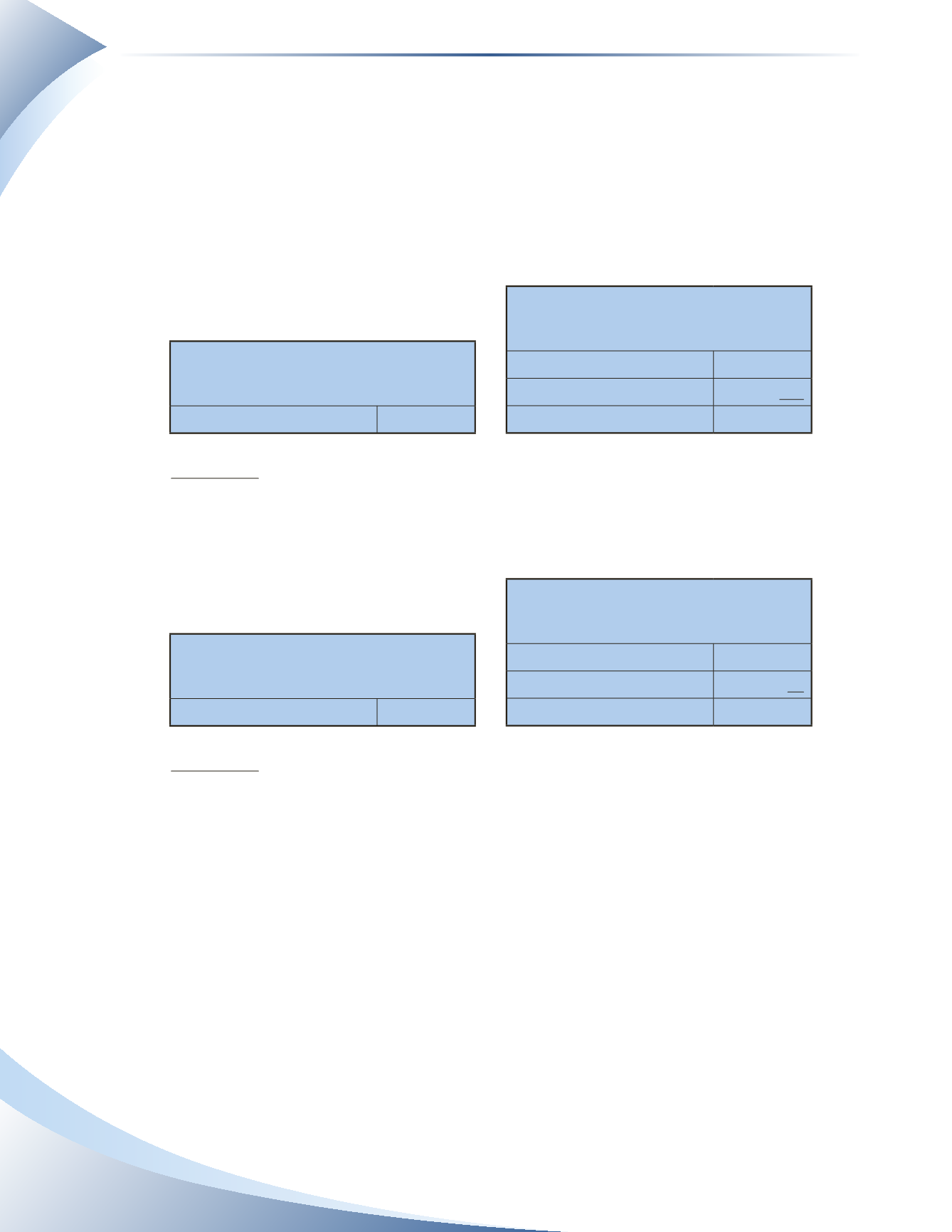

Jill Hanlon Retailer

January 31, 2016

General Ledger

Accounts Receivable

$1,591

Control account in the general ledger

The total of all subledger accounts

Jill Hanlon Retailer

Schedule of Accounts Receivable

January 31, 2016

Joe Blog

$635

Furniture Retailers

956

Total Accounts Receivable

$1,591

figure 9.20

A similar listing can be done for the accounts payable subledger. From Figure 9.19, the balance of

accounts payable was $80.The total of the accounts payable subledger is shown below.

Jill Hanlon Retailer

January 31, 2016

General Ledger

Accounts Payable

$80

Control account in the general ledger

The total of all subledger accounts

Jill Hanlon Retailer

Schedule of Accounts Payable

January 31, 2016

Antonio’s Electric

$0

Doug’s Maintenance

80

Total Accounts Payable

$80

figure 9.21

If the comparison of the general ledger control account and the total of the subledger accounts

shows that they do not balance, the difference must be investigated.The difference must be resolved

before the trial balance can be completed.

Returns

The special journals are designed to record specific types of transactions, but some transactions that

must be recorded do not fit into these special journals. As mentioned earlier, if a transaction does

not belong in one of the special journals, it must be recorded in the general journal. For example,

sales and purchase returns do not fit into the special journals and must be recorded in the general

journal.The only change to the way these transactions are recorded from what we learned earlier is

how the posting is processed for accounts receivable or accounts payable.