Introduction

ix

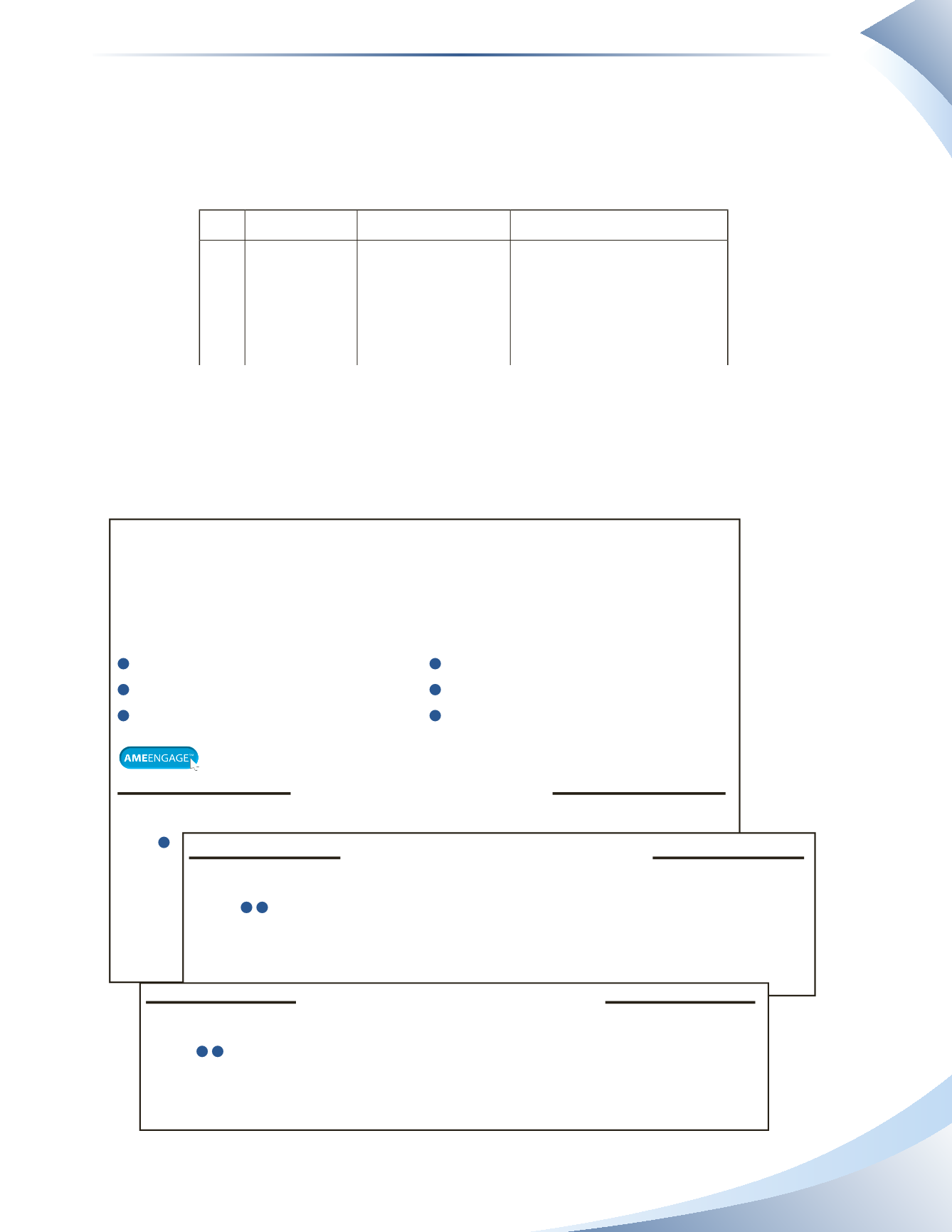

In addition to the Review Exercise solutions in the appendix, you will also find a handy chart to

illustrate some key differences between ASPE and IFRS organized by chapter and topic.

436

Appendix III

Review Exercise Solutions

Appendix III

ASPE VS IFRS

Chapter

Topic

Accounting Standards for

Private Enterprises (ASPE)

International Financial Reporting

Standards (IFRS)

3

When to use

• Private organization (sole

proprietorship, partnership,

private corporations)

• No plans to become public in

the near future

• ASPE also used by most

competitors

• Public corporation or owned by a public

company

• Private organization intending to become

public in the near future

• IFRS already adopted by most competitors

• Private enterprises adopting IFRS by choice

for other reasons, such as, in anticipation

of a bank's requirement for IFRS-based

financial statements in loan application

Cost

Less costly and simpler to

implement

Can be costly to implement

Number of disclosure

requirements

Fewer disclosures are required More disclosures are required

Comparability

Less comparable on a global

scale

More relevant, reliable and comparable on a

global scale

Development status ASPE may eventually evolve

into IFRS in the future

IFRS is positioned to be the global

accounting standards for the foreseeable

future

Level of judgments

required

More specific rules; fewer

judgments required

Fewer hard-and-fast rules; more judgments

required

5 Frequency of financial

statement issuance

Companies are required to

prepare financial statements

at least once a year. This

implies that the end-of-period

adjustments process must also

be completed at least once a

year.

Companies are required to prepare financial

statements at least once per quarter. This

implies that the end-of-period adjustments

process must be completed at least four

times a year.

6

Balance Sheet

or Statement of

Financial Position

terminology

The term "Balance Sheet" is

more often used, although the

term "Statement of Financial

Position" is also allowed.

The term "Statement of Financial Position"

is more often used, although the term

"Balance Sheet" is also allowed.

Order of items listed

on the balance sheet

or statement of

financial position

The listing order of items on a

balance sheet is not specified,

although ordering items from

most liquid to least liquid

on the balance sheet is a

common practice among the

companies adopting ASPE.

IFRS also does not prescribe the listing order

of items on a statement of financial position.

However, a common practice among the

companies adopting IFRS, particularly

European companies, is ordering assets

from least liquid to most liquid. Additionally,

equity is commonly presented before long-

term liabilities, followed by current liabilities.

7 Expense classification

on income statement

A company can choose to

present its expenses on an

income statement by nature,

or by function, or even by

using a mixture of nature and

function.

Expenses can be classified either by nature

or by function on an income statement.

Using a mixture of nature and function is

prohibited.

The workbook is comprised of assessment and application questions.

• Assessment questions (AS) are designed to test theory and comprehension of topics.

• Application questions (AP) are split into Group A and Group B problems. These questions test the

ability to perform the accounting functions, such as creating journal entries and financial statements.

Chapter 4

The ACCounTing CyCle: JournAls And ledgers

Assessment Questions

As-1 (

1

)

What does the term debit refer to?

A debit is an entry on the left side of a T-account.

As-2 (

1

)

True or False: A credit will always be an increase to any account.

False: A credit is the right side of the T-account. It can increase or decrease the account,

depending on the type of account.

As-3 (

1

)

Which three types of accounts use the debit side of the T-account to increase their value?

Assets, owner’s drawings and expenses all use debits to increase their values.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

leArning ouTComes

1

Distinguish betwee debits and credits

2

Describe the accounting cycle

3

Explain how to analyze a transaction

4

Record transactions in the general journal

5

Post j urnal entries to the general ledger

6

Prepare a trial balance

Access

ameengage.com

for integrated resources including tutorials, practice exercises, the digital textbook

and more.

Chapter 4

The Accounting Cycle: Journals and Ledgers

Application Questions group A

AP-1A (

1

3

)

Esteem Fitness provides fitness services for its customers. During June 2016, Esteem Fitness

had the following transactions.

Jun 1

Sold one-month memberships to customers for $4,500 on account.

Jun 3

Received a telephone bill for $250 which will be paid next month.

Jun 6

Paid an employee’s salary of $1,200.

Jun 10

Received $3,000 cash from customers paying in advance for upcoming one-year

memberships.

Jun 15

Paid $6,000 cash in advance for six months of rent.

Jun 20

Received a $10,000 loan from the bank.

Jun 26

Purchased equipment with $8,000 cash.

required

Complete the table to analyze each transaction.

Chapter 4

The Accounting Cycle: Journals and Ledgers

Application Questions group B

AP-1B (

1

3

)

Have‐a‐Bash is owned by Shelly Fisher and provides party planning services. During April

2016, Have‐a‐Bash had the following transactions.

Apr 1

The owner inv sted $5,800 cash into the business.

Apr 4

Planned a party for a customer for $740. The customer will pay later.

Apr 6

Paid $600 cash for rent for the month.

Apr 8

Received a $370 telephone bill which will be paid later.