Chapter 4

The Accounting Cycle: Journals and Ledgers

80

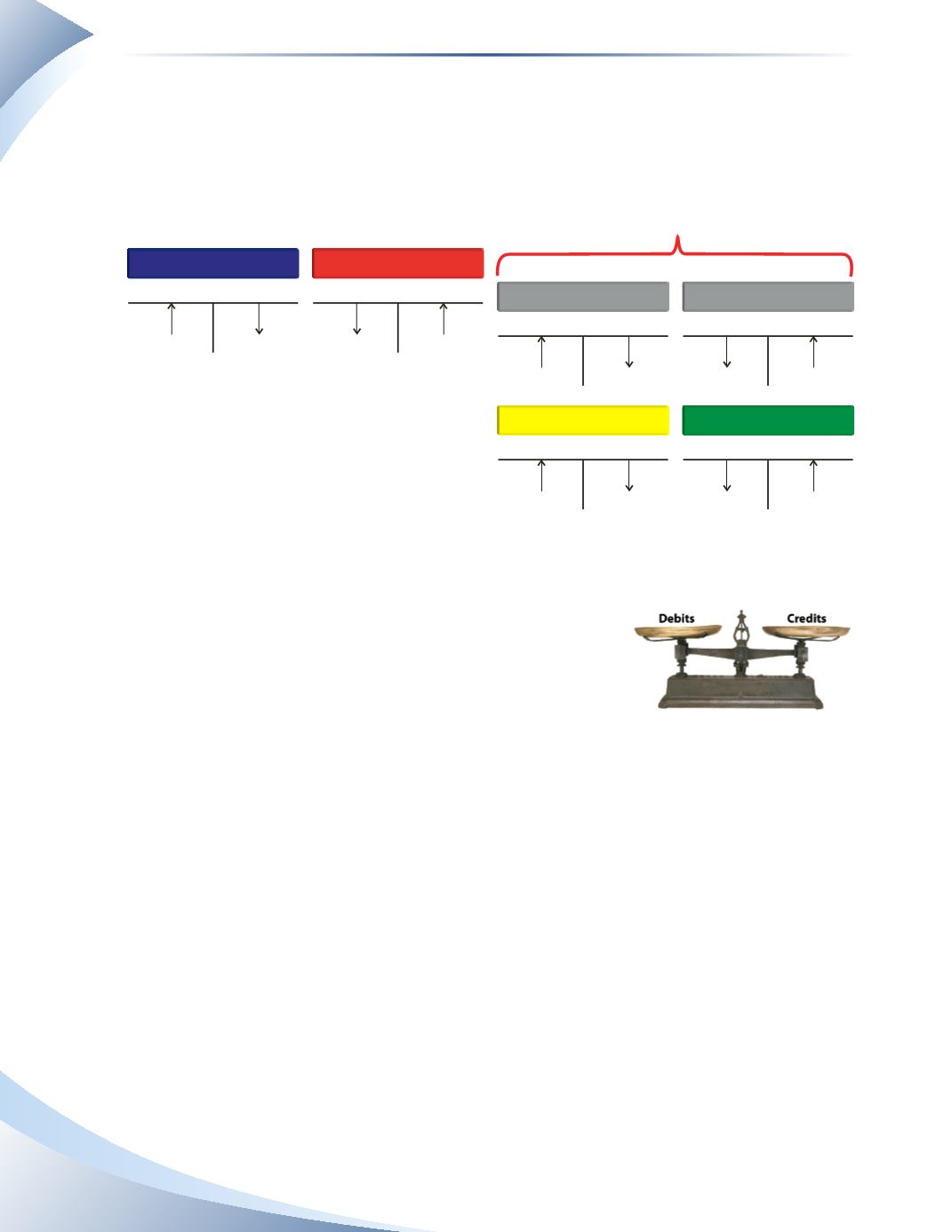

For the accounting equation to be correct and for the balance sheet to stay in balance, the total

value of the debits must always equal the total value of the credits. Use the Debit and Credit

Reference Guide shown in Figure 4.1 to help when analyzing transactions.

Debit and Credit Reference Guide

ASSETS

OWNER’S DRAWINGS

EXPENSES

OWNER’S CAPITAL

REVENUE

BANK LOAN

Increase

Increase

Increase

Increase

Owner’s Equity

Assets

=

+

Liabilities

Increase

Increase

Debit

Debit

Debit

Debit

Debit

Debit

Decrease

Decrease

Decrease

Credit

Credit

Credit

Decrease

Decrease

Decrease

Credit

Credit

Credit

________________

figure 4.1

Every transaction will have at least one debit and one credit.

The total of all debits in a transaction must equal the total of all

credits. If debits do not equal credits, the accounting equation

will not balance.

Each type of account also has a normal balance. A

normal balance

will correspond to the side

of the T-account that records the increase and is shown in bold in Figure 4.1. A normal balance

indicates a positive balance for the account. For instance, the cash account (an asset) has a debit

normal balance.

Using the Debit and Credit Reference Guide, let us look at a few sample transactions and see how

to translate increases and decreases into debits and credits.

1.

Provided services to a customer who pays cash.

2.

Paid cash to reduce the principal of the bank loan.

3.

Paid cash for a one-year insurance policy.

4.

Record maintenance expense, which will be paid later.