Chapter 4

The Accounting Cycle: Journals and Ledgers

82

Step 1

Step 2

Step 3

Step 4

Step 5

Step 6

Step 7

Step 8

Step 9

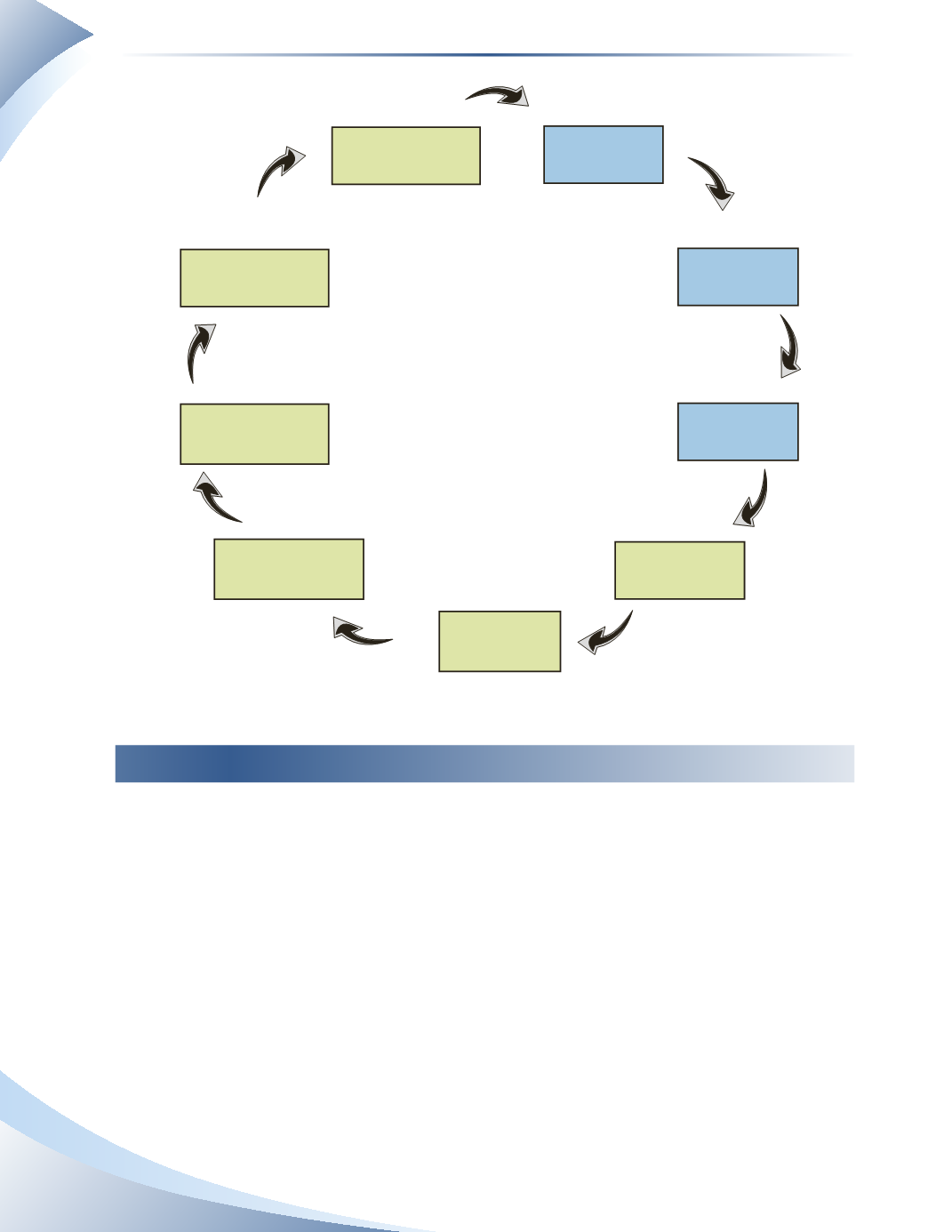

ACCOUNTING

CYCLE

Analyze

transactions

Journalize the

transactions

Post to ledger

accounts

Prepare the trial

balance

Journalize and

post adjusting

entries

Prepare the

adjusted trial

balance

Prepare the

financial

statements

Journalize and post

closing entries

Prepare the post-

closing trial balance

________________

figure 4.3

Analyze Transactions

The first part of the accounting cycle is to gather and analyze what must be recorded as trans-

actions. All transactions must have

source documents

or evidence that they actually happened.

Source documents can include sales receipts, bills, cheques, bank statements, etc.

As discussed earlier we must determine which accounts will be affected, what parts of the account-

ing equation the accounts belong to and identify whether these accounts will increase or decrease

as a result of this transaction. The extra step now is to match the increase or decrease of each ac-

count with a debit or credit entry to the account. Use the Debit and Credit Reference Guide in

Figure 4.1 to help with this.