Inventory: Merchandising Transactions

205

Chapter 7 Appendix

Appendix 7A: The Periodic Inventory System

As mentioned, the periodic inventory system determines the quantity of inventory on hand only

periodically. A physical count is taken at the end of the period to determine the value of the ending

inventory and cost of goods sold.

Thus, a periodic inventory system does not update the inventory account on a regular basis, only

when a physical count is taken. On a regular basis, the periodic inventory system updates a new list

of income statement accounts which are used to calculate cost of goods sold.

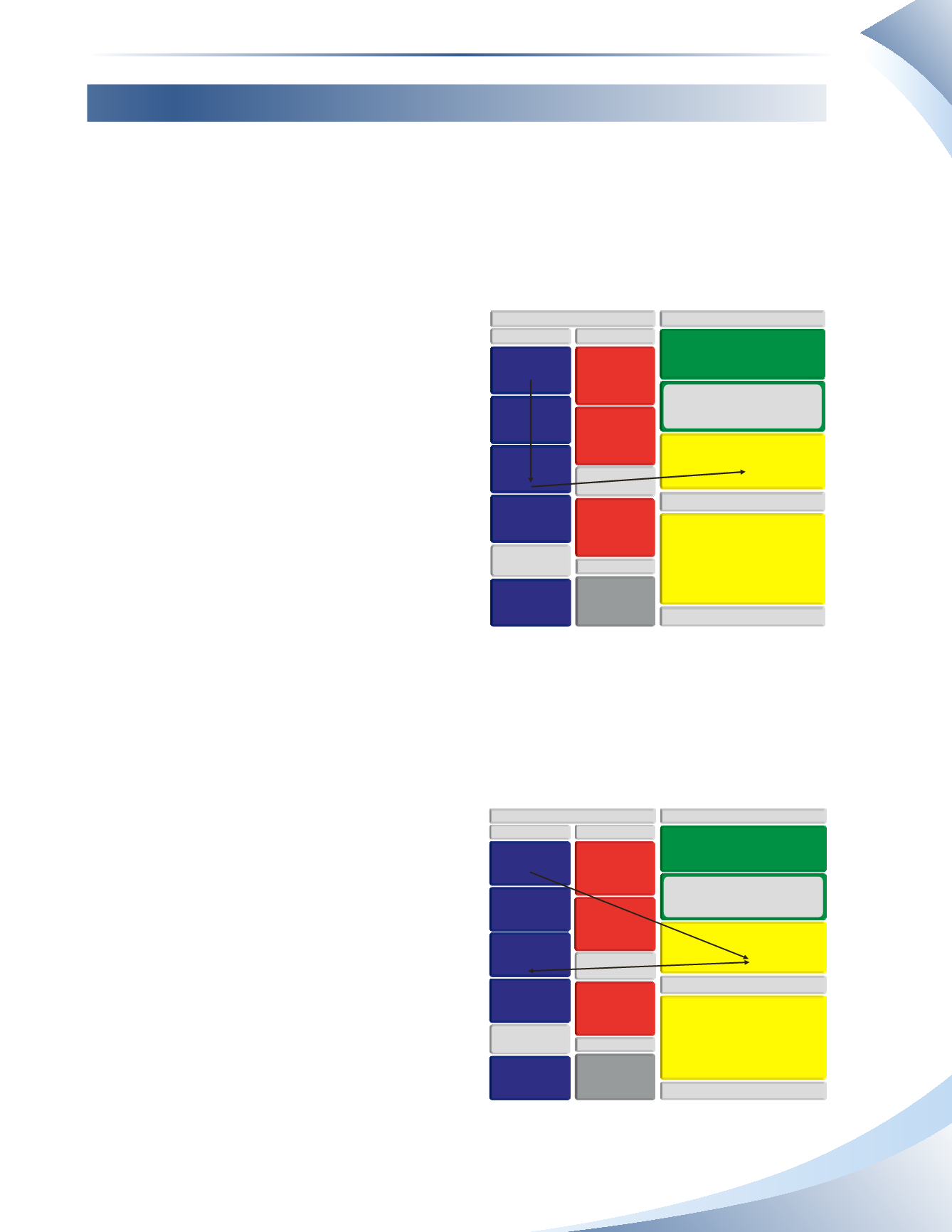

Consider the differences between the perpetual

and the periodic inventory system. Figure 7A.1

illustrates the perpetual inventory system. A

business that has the technology to properly

implement the perpetual inventory system will

record purchases, discounts, allowances and other

adjustments into the inventory asset account.

Inventory is then transferred to cost of goods

sold when a sale is made. Cost of goods sold is

immediately matched to sales and gross profit is

reported every month, although gross profit may

be slightly incorrect if an inventory count is not

performed.

A business that does not have the technology to

constantly update inventory like in the perpetual inventory system must instead use the periodic

inventory system. Figure 7A.2 illustrates the periodic inventory system. Inventory shows an

opening value at the beginning of the period, but is only adjusted up or down at the end of the

period when an inventory count is performed. All purchases, discounts, allowances and other

adjustments are recorded directly into the income statement as part of cost of goods sold.

If purchases were recorded in the inventory

account on the balance sheet, they would always

remain in inventory since inventory is not

transferred to cost of goods sold when a sale

is made. This would leave a large amount of

inventory remaining on the balance sheet and no

cost of goods sold on the income statement. It

is more practical to record purchases directly on

the income statement, and adjust the inventory

account only at year end.

Keep the concept of the periodic inventory system

in mind as the journal entries are presented.The

transactions are very similar to the perpetual

inventory system, except that income statement accounts are affected instead of inventory.

SALES RETURNS & ALLOWANCES

INCOME STATEMENT

GROSS PROFIT

OPERATING EXPENSES

SALES REVENUE

COST OF GOODS SOLD

BALANCE SHEET

OPERATING INCOME

CURRENT ASSETS

CASH

INVENTORY

ACCOUNTS

RECEIVABLE

PREPAID

EXPENSES

PROPERTY, PLANT

& EQUIPMENT

LONG-TERM

ASSETS

ACCOUNTS

PAYABLE

BANK LOAN

CURRENT LIABILITIES

UNEARNED

REVENUE

LONG-TERM

LIABILITIES

OWNER’S EQUITY

OWNER’S

CAPITAL

____________

figure 7A.1

SALES RETURNS & ALLOWANCES

INCOME STATEMENT

GROSS PROFIT

OPERATING EXPENSES

SALES REVENUE

COST OF GOODS SOLD

BALANCE SHEET

OPERATING INCOME

CURRENT ASSETS

CASH

INVENTORY

ACCOUNTS

RECEIVABLE

PREPAID

EXPENSES

PROPERTY, PLANT

& EQUIPMENT

LONG-TERM

ASSETS

ACCOUNTS

PAYABLE

BANK LOAN

CURRENT LIABILITIES

UNEARNED

REVENUE

LONG-TERM

LIABILITIES

OWNER’S EQUITY

OWNER’S

CAPITAL

____________

figure 7A.2