206

Inventory: Merchandising Transactions

Chapter 7

Appendix

Purchases

When inventory is purchased for resale using a periodic inventory system the inventory account

is not debited. Instead, we debit an account called purchases on the income statement, which is

part of cost of goods sold. If the inventory was paid for on credit, then accounts payable is credited.

If the inventory was paid for with cash, then the

cash account is credited. In this example, Tools 4U

purchased inventory of $10,000 on January 1, 2016.

Assume all purchases and sales are made on account.

The purchases account is a temporary account located on the income statement as part of COGS. It

records all the inventory purchased by a company during a specific period of time under the periodic

inventory system.

The values of inventory and cost of goods sold are not adjusted until the end of the period when

the physical inventory count is taken. As a result, we need to track the costs related to inventory in

separate accounts.

Purchase Returns

Continuing with the example of Tools 4U, assume the company returned $300 worth of inventory to

its supplier. Instead of just crediting the purchases account, businesses that use a periodic inventory

system track these returns by using a temporary

contra account to purchases called

purchase returns

and allowances

.This new account is also part of cost

of goods sold. The journal entry to record the above

return is shown in Figure 7A.4.

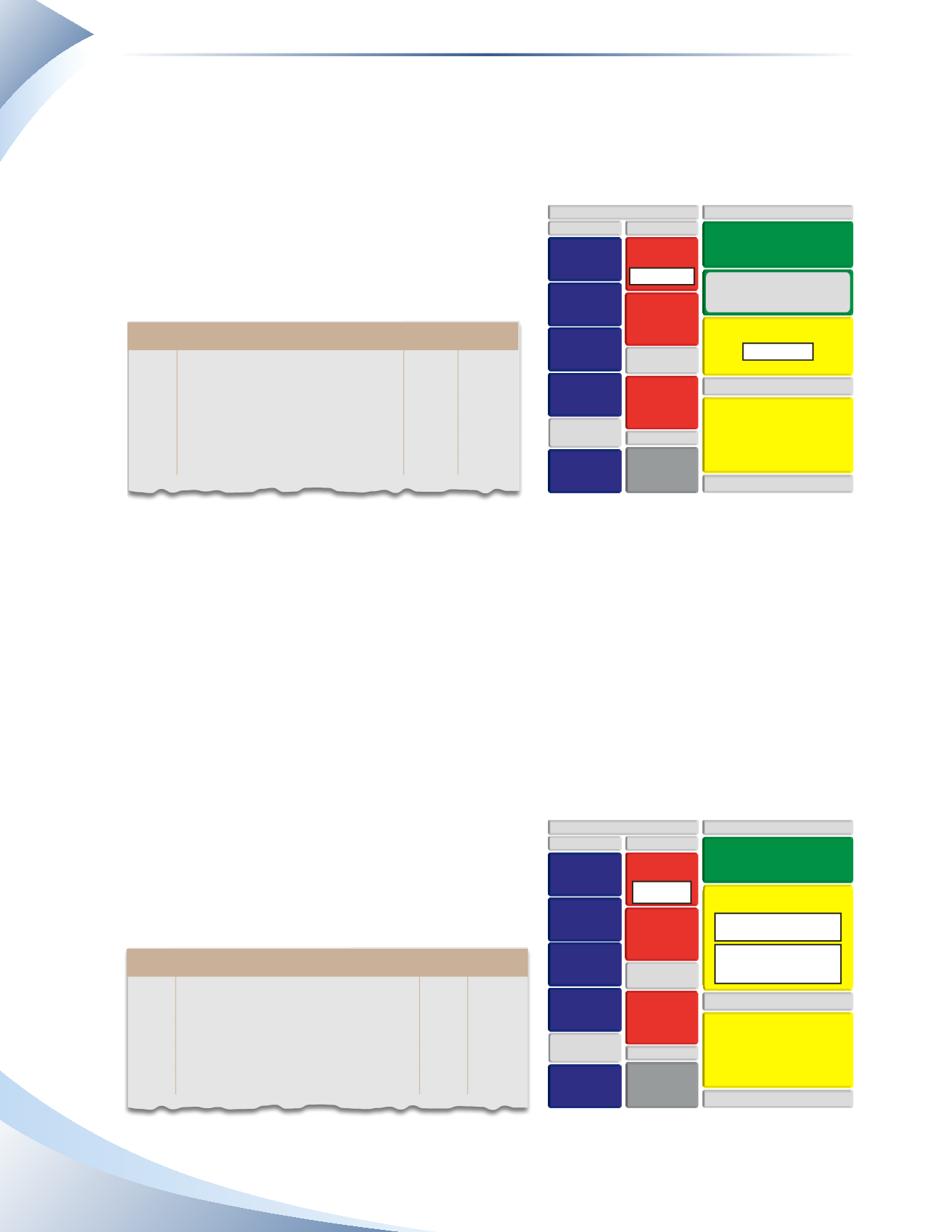

Journal

Page 1

date

2016

account title and explanation debit Credit

Jan 1 Purchases

10,000

Accounts Payable

10,000

Record purchase of inventory

____________

fIGuRe 7A.3

SALES RETURNS & ALLOWANCES

INCOME STATEMENT

GROSS PROFIT

OPERATING EXPENSES

SALES REVENUE

COST OF GOODS SOLD

BALANCE SHEET

CURRENT ASSETS

CASH

INVENTORY

ACCOUNTS

RECEIVABLE

PREPAID

EXPENSES

PROPERTY, PLANT

& EQUIPMENT

LONG-TERM

ASSETS

ACCOUNTS

PAYABLE

BANK LOAN

CURRENTLIABILITIES

UNEARNED

REVENUE

LONG-TERM

LIABILITIES

OWNER’S EQUITY

OWNER’S

CAPITAL

+ $10,000 CR

+ $10,000 DR

OPERATING INCOME

INCOME STATEMENT

GROSS PROFIT

OPERATING EXPENSES

SALES REVENUE

COST OF GOODS SOLD

BALANCE SHEET

CURRENT ASSETS

CASH

INVENTORY

ACCOUNTS

RECEIVABLE

PREPAID

EXPENSES

PROPERTY, PLANT

& EQUIPMENT

LONG-TERM

ASSETS

ACCOUNTS

PAYABLE

BANK LOAN

CURRENTLIABILITIES

UNEARNED

REVENUE

LONG-TERM

LIABILITIES

OWNER’S EQUITY

OWNER’S

CAPITAL

OPERATING INCOME

$10,000 CR

– $300 DR

PURCHASES

$10,000 DR

PURCHASE RETURNS

& ALLOWANCES

+ $300 CR

Journal

Page 1

date

2016

account title and explanation debit Credit

Jan 2 Accounts Payable

300

Purchase Returns and Allowances

300

Record purchase returns

____________

fIGuRe 7A.4