258

Chapter 9

Accounting Information Systems

lists all the company’s accounts and its corresponding balances.The main purpose of a trial balance

is to ensure that all debits equal all credits. The trial balance may need to be adjusted (e.g. to

take into account recognition of prepaid expenses, depreciation of assets, etc.) before the financial

statements are produced. The financial statements are then organized into a financial report for

management to review.

________________

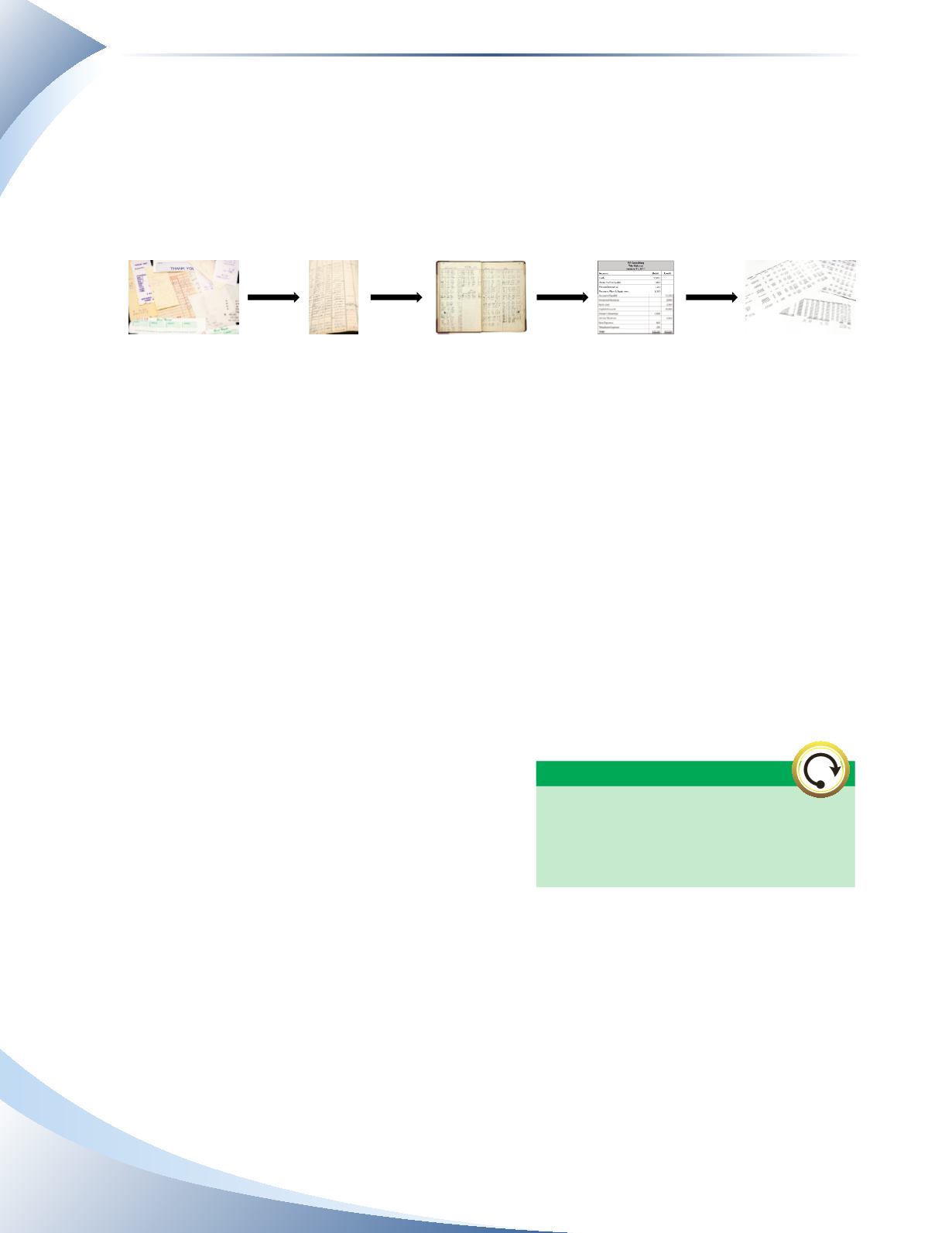

figure 9.1

The Traditional Accounting Paper Trail

Source Documents

Journal

General Ledger

Financial Reports

Trial Balance

Regardless of whether one is dealing with a manual or a computerized system, an effective

accounting system should ensure

• Adequate internal controls to prevent misuse of assets

• Accurate information is provided on a timely basis

• Effective communication across the various components of the system

• Flexibility to allow for changes as the organization grows and evolves

• Maximum benefits at a reasonable cost

In this section, we will focus on two components of the traditional accounting information system:

special journals and subsidiary ledgers.

Special Journals

Following the manual accounting paper trail, after the source documentation has been received,

the next step for the accountant is to record the

transaction in journal format.

In a traditional accounting system, recording all

business transactions in one journal could be very

time consuming—especially when there are lots

of activities concerning specific transactions. For

transactions that occur regularly, it is wise tomaintain

a separate book called a

special journal

. Examples of regular transactions include sales, purchases,

cash payments, cash receipts and payroll. These journal entries are essentially the same entries

already covered, except we will sort them by type and condense the amount of information to be

recorded. Maintaining these events in a separate set of books will allow easy access to information

pertaining to these activities. For example, if a sales manager wants to see the amount of credit sales

generated in May, she could examine the sales journal and add up all the sales for that month. In

other words, accounting information is organized into specific categories so that people can look

back later and easily extract information. Examples of special journals include

Sales Journal:

This journal is used to record all sales made on account.

All transactions must be recorded in a

journal before being posted to the ledgers,

regardless of whether special journals are

used or not.

WORTH REPEATING