263

Chapter 9

Accounting Information Systems

Companies often offer sales discounts to their customers (i.e. 2/10, n/30). The terms of each sale

should be recorded in the sales journal. However, if a company provides the same sales terms to all

its customers, there is no need to record the terms in the sales journal.

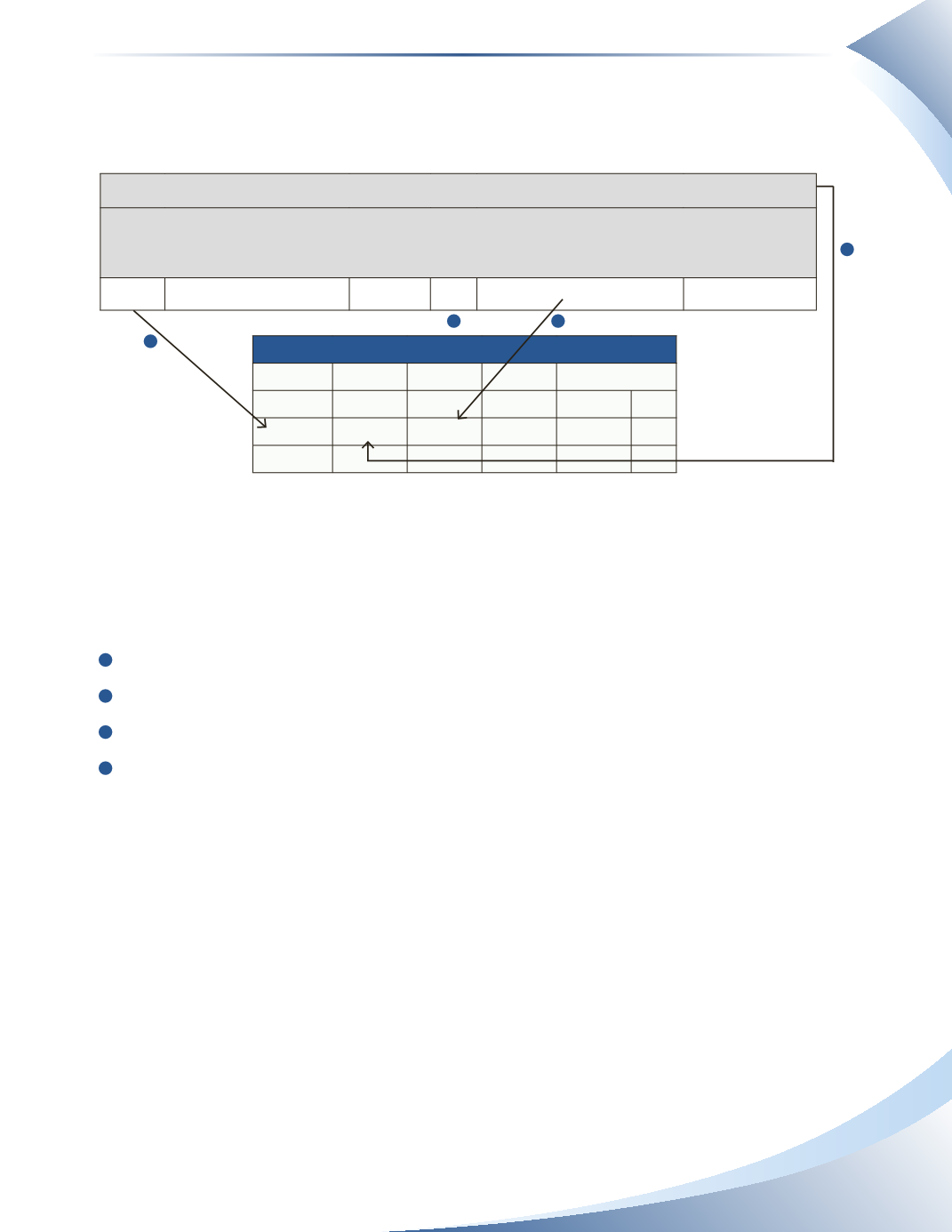

Sales Journal

Page 1

Date

Account

Invoice # PR

Accounts Receivable/Sales

(DR/CR)

COGS/Inventory

(DR/CR)

Jan 5 Joe Blog

5125

1,235

1,100

Account:

Joe Blog

Date

PR

DR

CR

Balance

2016

Jan 5

SJ1

1,235

1,235 DR

________________

figure 9.5

At the end of the month, the totals of all the columns are posted to the appropriate ledger accounts.

The numbers in brackets under the totals represent the ledger numbers of the accounts used. In this

example, we are focusing on accounts receivable, account number 110. The posting to the accounts

receivable control account in Figure 9.6 follows these steps.

1

Transfer the date from the sales journal to the date column in the ledger account.

2

Make a note of the journal and page number in the PR column of the ledger.

3

Transfer the total of the accounts receivable column to the debit column in the ledger account.

4

Indicate the posting is complete by writing the general ledger number under the total.

1

3

2

4