268

Chapter 9

Accounting Information Systems

A purchase of an item that does not have a heading in the journal is placed in the Other column.

Suppose the company received an invoice for $80 of maintenance done for the office. The $80 is

placed in the Other column and in the Accounts Payable column. Since the amount in the Other

column must be posted immediately to the general ledger to the maintenance expense account,

the GL number is placed in the PR column. Additionally, since the $80 must also be posted to

the accounts payable subledger, a check mark is placed in the PR column.

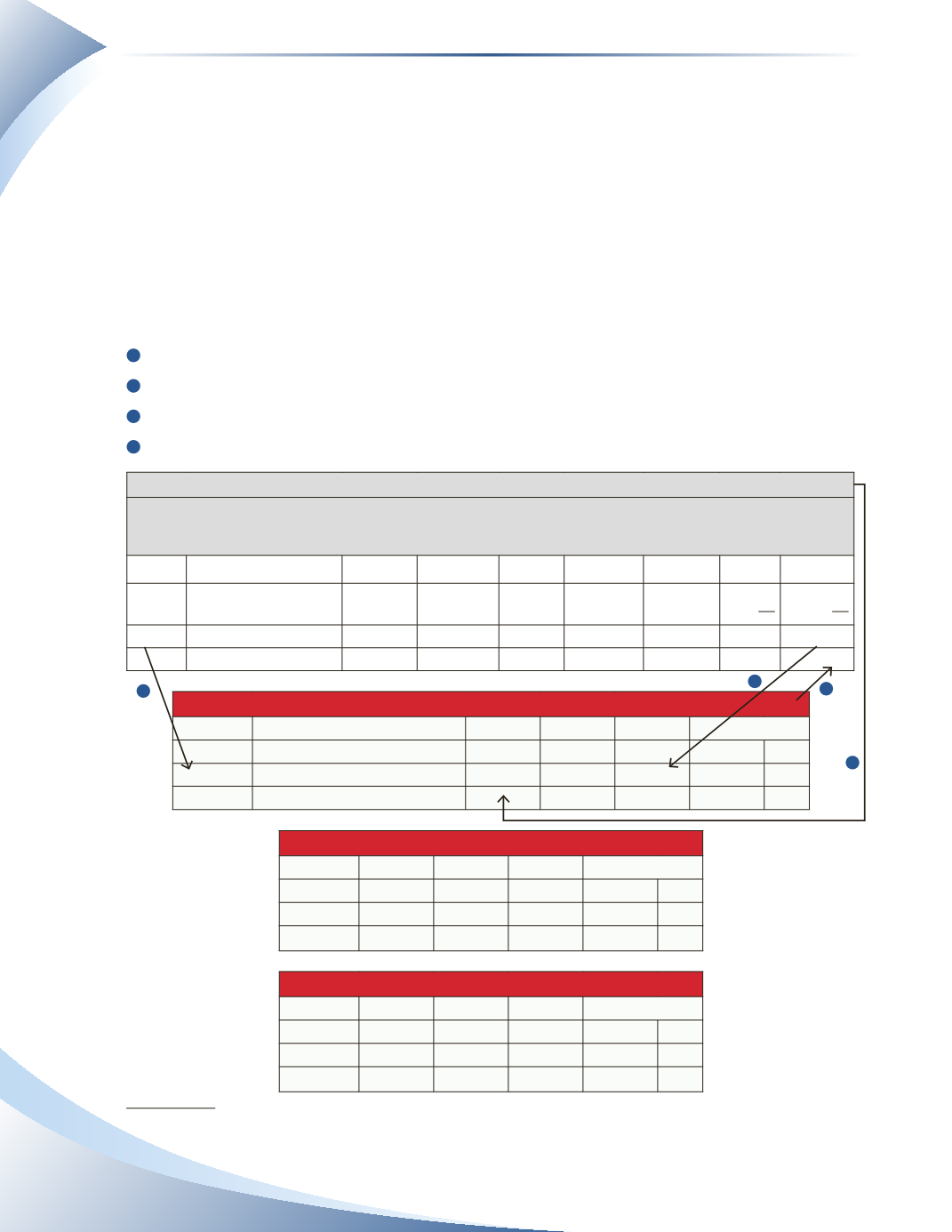

At the end of the month, the totals of the columns are posted to the general ledger accounts.The

posting of the accounts payable is shown in Figure 9.14. The totals of the individual subledger

accounts must equal the balance of the accounts payable control account. The posting to the

accounts payable control account follows these steps.

1

Transfer the date from the purchases journal to the date column in the ledger account.

2

Make a note of the journal and page number in the PR column of the ledger.

3

Transfer the total of the accounts payable column to the credit column in the ledger account.

4

Indicate the posting is complete by writing the general ledger number under the total.

Purchases Journal

Page 6

Date

Account

Invoice # Terms

PR

Inventory

(DR)

Office

Supplies

(DR)

Other

(DR)

Accounts

Payable

(CR)

Jan 3 Antonio's Electric

2089 3/15, n 30

4,200

4,200

Jan 19 Maintenance Expense/

Doug’s Maintenance

6091

525/

80

80

Jan 31 Total

$4,200

$80 $4,280

(120)

(X)

(200)

Account:

Accounts Payable

GL. No.

200

Date

Description

PR

DR

CR

Balance

2016

Jan 31

PJ6

4,280 4,280 CR

Account:

Antonio's Electric

Date

PR

DR

CR

Balance

2016

Jan 3

PJ6

4,200 4,200 CR

Account:

Doug’s Maintenance

Date

PR

DR

CR

Balance

2016

Jan 19

PJ6

80

80 CR

figure 9.14

1

3

4

2