Chapter 1

Financial Statements: Personal Accounting

21

The list of transactions is numbered and will be numbered in the T-accounts to help keep track of

the transactions. Recall that the accounting equation must balance, so every transaction will affect

at least two accounts.

The Process

1

If applicable, enter the opening balances in the appropriate T-account. Then check that the

accounting equation is in balance before you begin entering transactions. This step is high-

lighted for the opening balance of the cash account in the T-account worksheet.

2

Enter both sides of the transaction in the correct account in the balance sheet and/or income

statement. Be sure to record the transaction number so that you may check your work.This step

is highlighted for the first transaction in the T-account worksheet.

3

Calculate the totals of the T-accounts on the income statement and calculate the surplus or

deficit. A surplus will increase net worth and a deficit will decrease net worth.

4

Calculate the totals of the T-accounts on the balance sheet and complete the accounting equa-

tion at the bottom of the balance sheet to check that it balances.

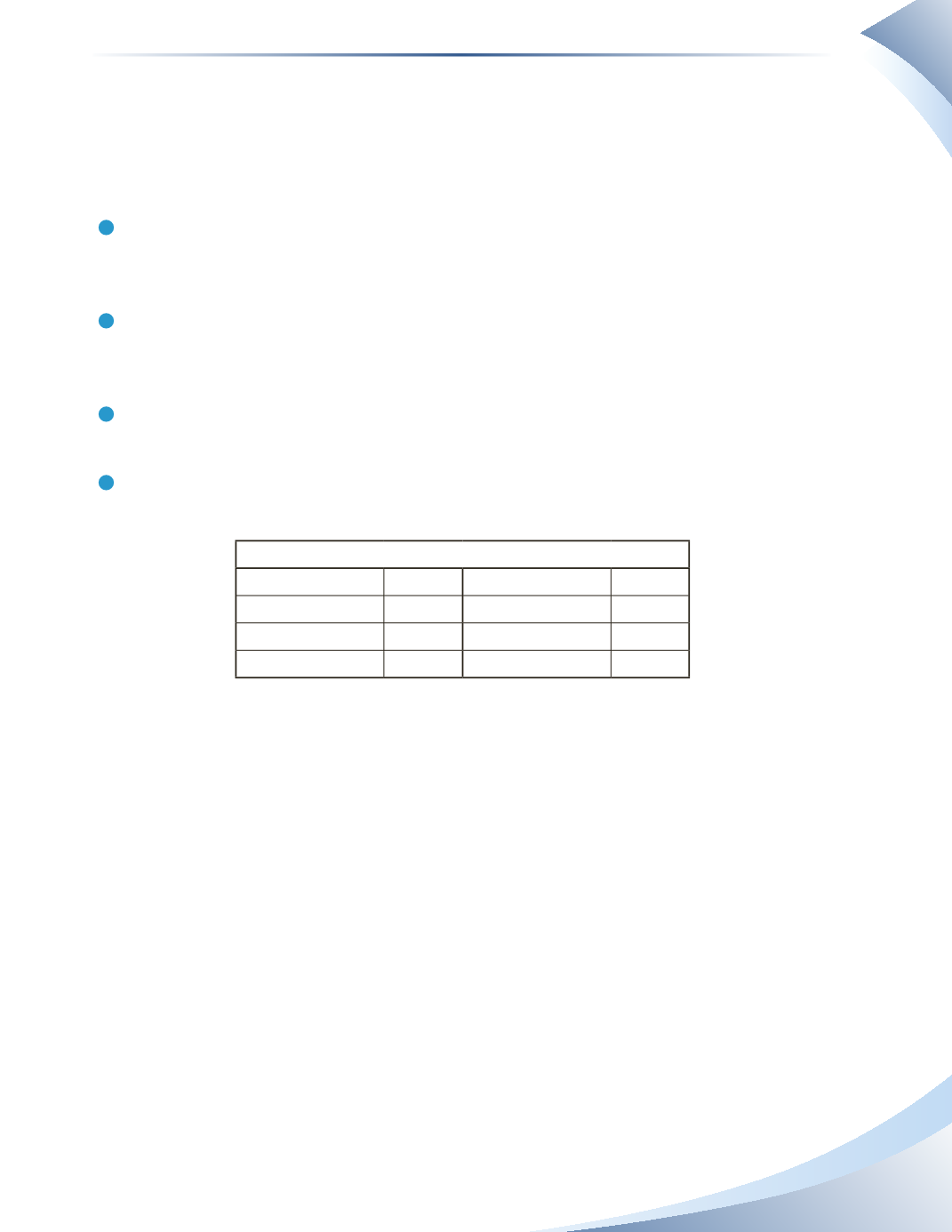

Opening Balances as at April 1, 2016

Cash

$1,000 Unpaid Accounts

$1,500

Prepaid Insurance

0 Mortgage

90,000

Contents of Home

6,000 Bank Loan

0

House

150,000 Net Worth

65,500

Transactions

1. Earned and deposited salary of $2,500.

2. Paid $1,200 cash for a one-year insurance policy.

3. Paid for $150 of entertainment with credit card.

4. Received a $4,000 loan from the bank.

5. Won $800 in a lottery.

6. Paid $1,000 for mortgage. Interest is $100 and the remainder is the principal.

7. Purchased new furniture worth $1,400 with credit card.

8. Bought food with $400 cash.