Chapter 2

Linking Personal Accounting to Business Accounting

39

accounts of the business when the invoice is received from the supplier.

Equity decreases and it is recorded as an expense on the income

statement,which also decreases net income.Remember that recognizing

an expense results in a decrease to equity.

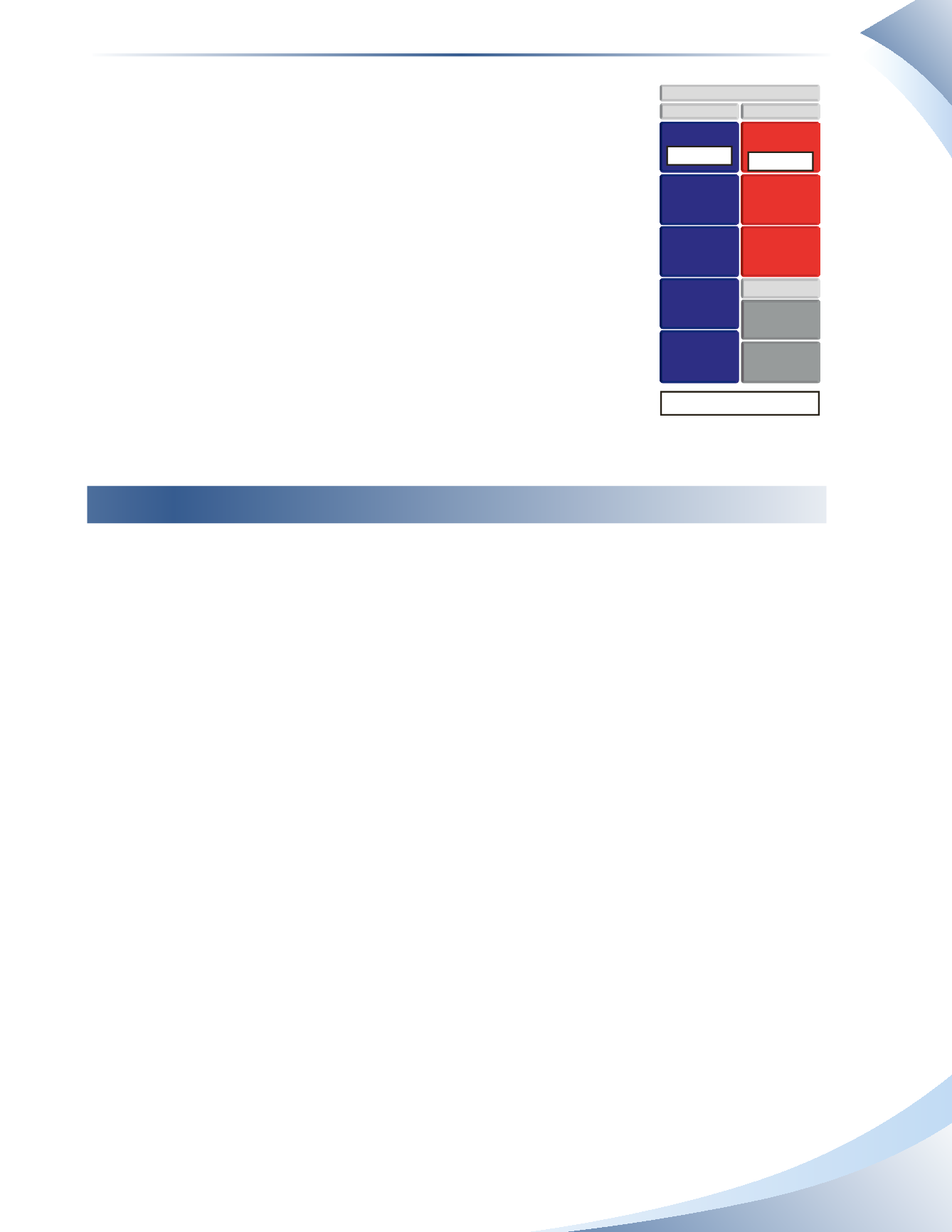

Now assume that two months have passed and the business pays the

$700 owed to the maintenance supplier. Figure 2.16 illustrates the

accounting impact of this transaction.This transaction is often referred

to as a “payment of account.” Equity does not change. Only an asset

(cash) and a liability (accounts payable) are affected.

Business Transactions

The ultimate goal of recording business transactions is to be able to create financial statements

and assess how well the business is performing. However, not everything the business does will

be recorded in the T-accounts and appear on the financial statements. A transaction occurs when

the business trades something of value with another person or business and this causes a change

in assets, liabilities or equity.The thing of value could include services, products, cash, a promise to

pay money, or the right to collect money.

An

event

, on the other hand, does not involve trading something of value. Since assets, liabilities

and equity are not affected by an event, nothing is recorded in the T-accounts. An event can lead

to a transaction at a later date, but it is only at that later date that anything would be recorded in

the T-accounts. For example, signing a contract with a customer to provide service in two months’

time is an event. At the signing, nothing of value has been traded, therefore nothing is recorded in

the T-accounts. However, two months later after the services have been provided, a transaction has

occurred and will be recorded in the T-accounts.

We will examine several business transactions and how they are recorded in the T-accounts. Keep

in mind that every transaction must leave the accounting equation in balance, so every transaction

must be recorded in at least two accounts. We will explain each transaction and illustrate how the

transaction will be recorded in the T-accounts. We will also illustrate how the accounting equation

will remain in balance and explain any changes to equity.The reason for the change to equity will be

listed under the explanation column and will be colour coded to match revenue, expense or equity

accounts. If there is no change to equity, the explanation column will remain empty.

2

ASSETS

BALANCE SHEET

LIABILITIES

CASH

ACCOUNTS

RECEIVABLE

PROPERTY, PLANT

& EQUIPMENT

PREPAID

EXPENSES

OFFICE

SUPPLIES

ACCOUNTS

PAYABLE

UNEARNED

REVENUE

BANK

LOAN

- $700

- $700

OWNER’S EQUITY

OWNER’S

CAPITAL

OWNER’S

DRAWINGS

No change in owner’s equity

______________

FIGURE 2.16