Chapter 10

Cash Controls

305

ACCOUNTS

RECEIVABLE

ACCOUNTS

PAYABLE

INVENTORY

ASSETS

BALANCE SHEET

LIABILITIES

CASH

OWNER’S EQUITY

UNEARNED

REVENUE

LOANS

PAYABLE

–

$360 CR

+

$360 DR

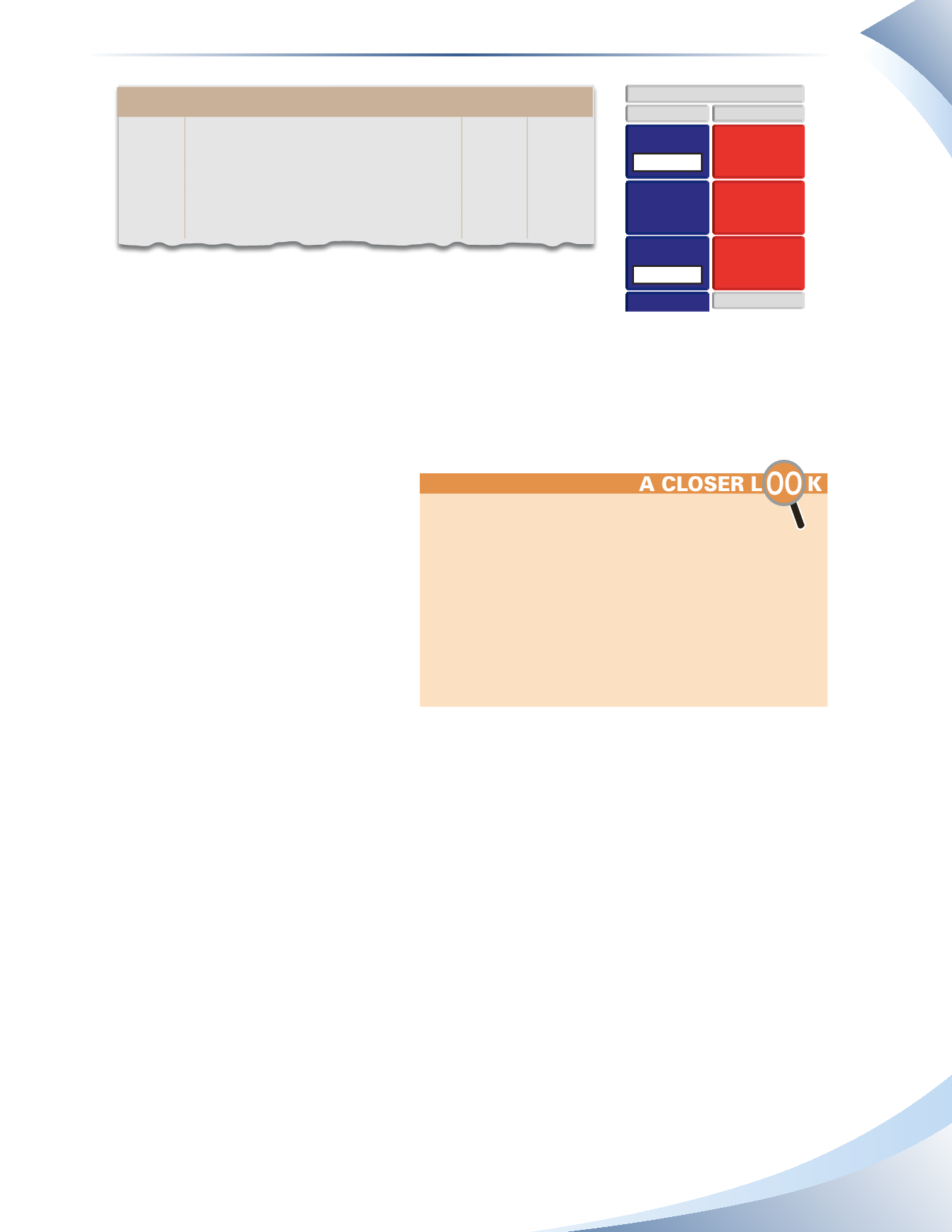

Journal

Page 1

Date

2016

account title and explanation

Debit Credit

Jun 30 Cash

360

Inventory

360

Correct error in ledger

______________

FIGURE 10.22

When an error is made by the bookkeeper, the bookkeeper must go back into the records to

determine what the original entry was for. This will determine which account will be used to

offset the cash account. In our example, the payment was for inventory. If the payment was to

pay off an account, use accounts payable; if it was to pay this month’s rent, use rent expense; if it

was to pay a telephone bill, use telephone expense, etc.

As with the previous examples, any

discrepancy between the bank statement

and the ledger record should be examined

and then corrected with the appropriate

entries.

Incorrect amounts in the ledger can be

more or less than the amounts shown

on the bank statement. Each error must

be analyzed carefully for appropriate

adjustments.

Bank reconciliation summary

Once all the items on a bank statement and the ledger have been matched up, only a few items

should remain that need to be reconciled. Figure 10.23 summarizes how items will be treated on a

bank reconciliation. Remember that all items that must be added to or subtracted from the ledger

balance must be recorded in a journal entry.

In a computerized accounting system, errors in the

ledger, such as the one described in Figure 10.22, are

corrected using two entries instead of one. The first

entry would be a $950 debit to cash and a $950 credit to

inventory. This entry reverses the original incorrect entry.

The second entry would be a $590 debit to inventory

and a $590 credit to cash to record the correct amount

of the June 3 cheque. The net result is the same as the

single entry in the amount of $360 shown above. Manual

accounting systems may not use this method because it

requires more entries and provides more room for error.